Decentralized Wireless Access Network

2.3 DeWi

The broadband wireless access network is the most desirable development target for DePIN, as this type of network supports most people's daily telecommunication needs. With the challenges of 5G roll-out, it has become a hot sector in DePIN, and has been called Decentralized Wireless, or DeWi. This DePIN subsector often includes projects deploying narrow band wireless access networks as well.

The traditional capital-intensive, top-down model telcos use to build networks is unsuitable for building 5G networks, which requires significantly more base stations than older generation networks. This level of deployment has proven to be economically infeasible for telcos. Besides the large number of base stations, other issues like high site acquisition costs, complex and expensive wireless spectrum purchasing procedures, surprising electricity bills, challenges in mobilizing thousands of field technicians to install and maintain complex equipment, and the staggering affordability of the general public, all limit 5G deployment under centralized network deployment models.

In contrast, DeWi’s flywheel and open access-deployment business model can empower individuals and businesses to improve their connectivity and add wireless density where it is not financially feasible for traditional telcos or other network operators to do so. For example, the owner of a restaurant with historically bad connectivity could deploy their own DeWi equipment, solving their connectivity problem for themselves and their customers. While it’s highly unlikely that DeWi completely replaces traditional networks, the two can coexist with one another and develop a symbiotic relationship.

However, enabling a true decentralized infrastructure remains challenging, as this industry is conventionally dominated by Telcos and influential telecom equipment vendors. Complex telecommunication equipment is needed, and only well trained engineers and technicians can operate and maintain it. Interoperability and vendor dependency are big difficulties for telcos, and have set obstacles for decentralized telco concepts. The O-RAN, or Open Radio Access Network (O-RAN, OpenRAN), is a network design concept intended to improve the interoperability and standardization of RAN elements via a unified interconnection standard for white-box hardware and open source software elements from different vendors. OpenRAN ’s mission is to accelerate innovation and commercialization in the RAN domain with multi-vendor interoperable products and solutions that are easy to integrate within the operator’s network, and that are verifiable for different deployment scenarios. O-RAN architecture integrates a modular base station software stack with off-the-shelf hardware, which allows baseband and radio unit components from discrete suppliers to operate seamlessly together. In addition, 5G provides a cloud native architecture where the key network functions are managed via cloud and edge computing, which can be carried out by off-the-shelf computers

rather than dedicated telco equipment. These initiatives and efforts have paved the way for a true decentralized network.

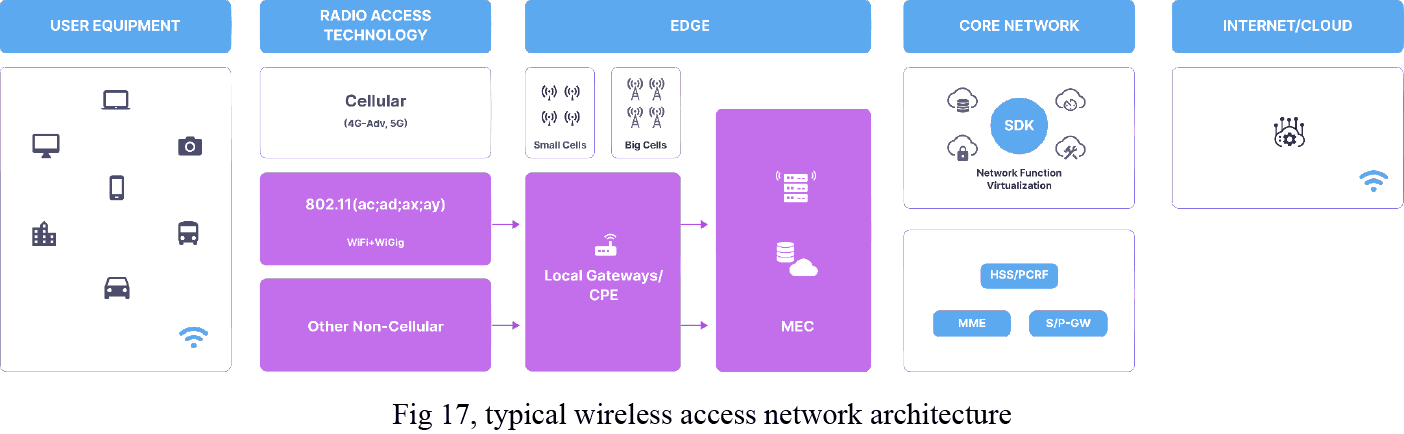

In the diagram above, WiFi and Cellular are represented by two parallel radio access networks, and the data traffic merges at the edge of the network. Since the release of iOS 7, most mobile phones have supported Hotspot 2.0 (formerly Passpoint), which is also supported by nearly all WiFi chips released since 2016. This allows for WiFi off-loading and in fact, (per Section 1.1) WiFi carries more data traffic than cellular networks.

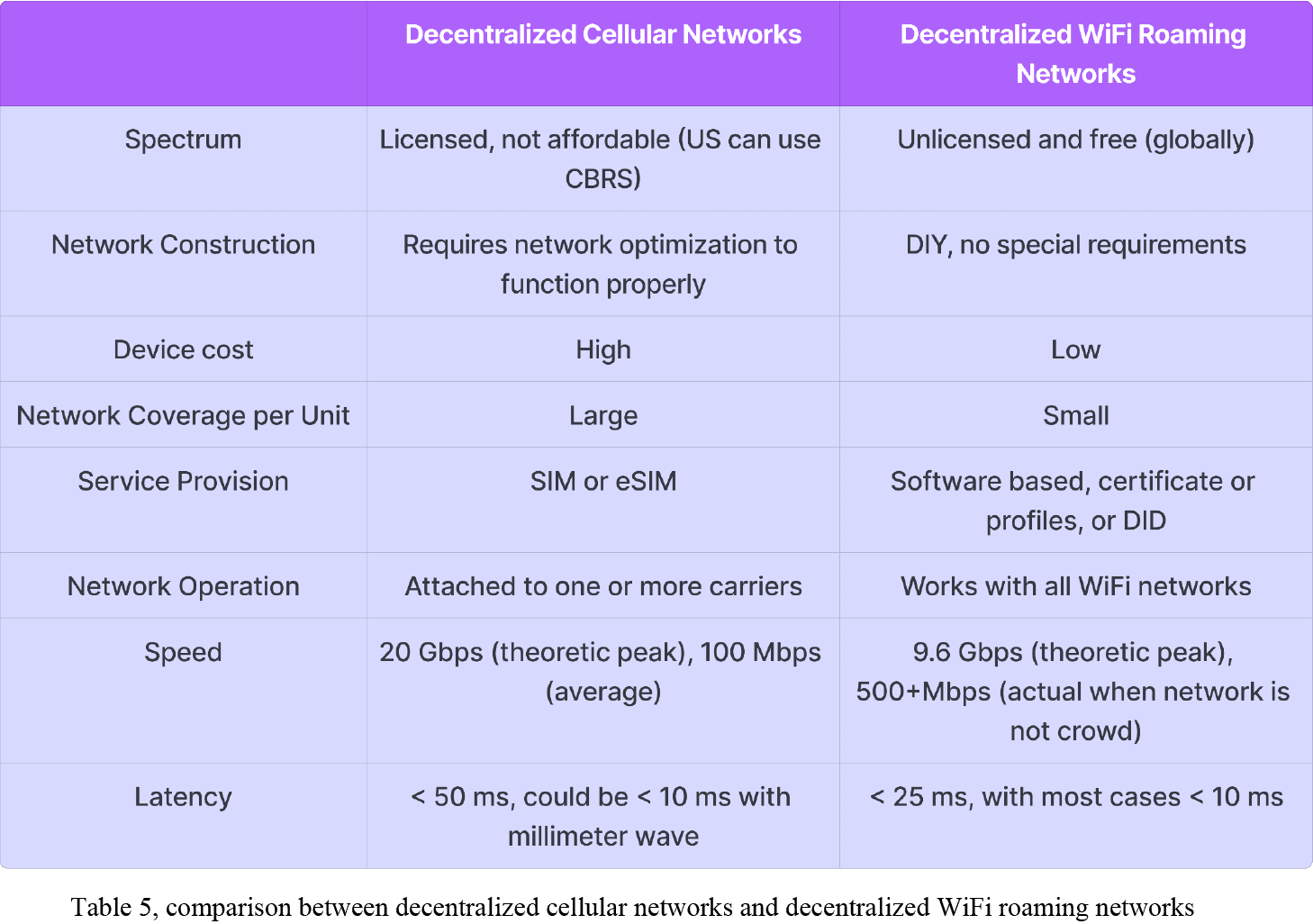

The table below compares the decentralized cellular network with the decentralized WiFi roaming network. As it and the following figures indicate, the key network performance between 5G and WiFi are somewhat similar.

From the perspective of decentralized networks, the main challenge for cellular-based networks is the huge barrier set by the existing industrial players and even governments. Decentralized operators cannot acquire the necessary spectrum resources, and must piggyback on other carriers' networks except for the CBRS, which is a 150 MHz wide broadcast band of the 3.5 GHz band (3550 MHz to 3700 MHz) available in the United States only. While the precise spectrum allocations may be different than CBRS, countries like Germany, Brazil, UK and Japan will allow for the same privatization of public radio services. However, an auction must be expected. The number of relevant equipment vendors are also limited due to high entry barriers, and they typically work only with large enterprises, while SIM and eSIM are still highly regulated. The need for network optimization is another challenge unless the decentralized operators can come up with a way to reward people to conduct field services which are inherently off-chain.

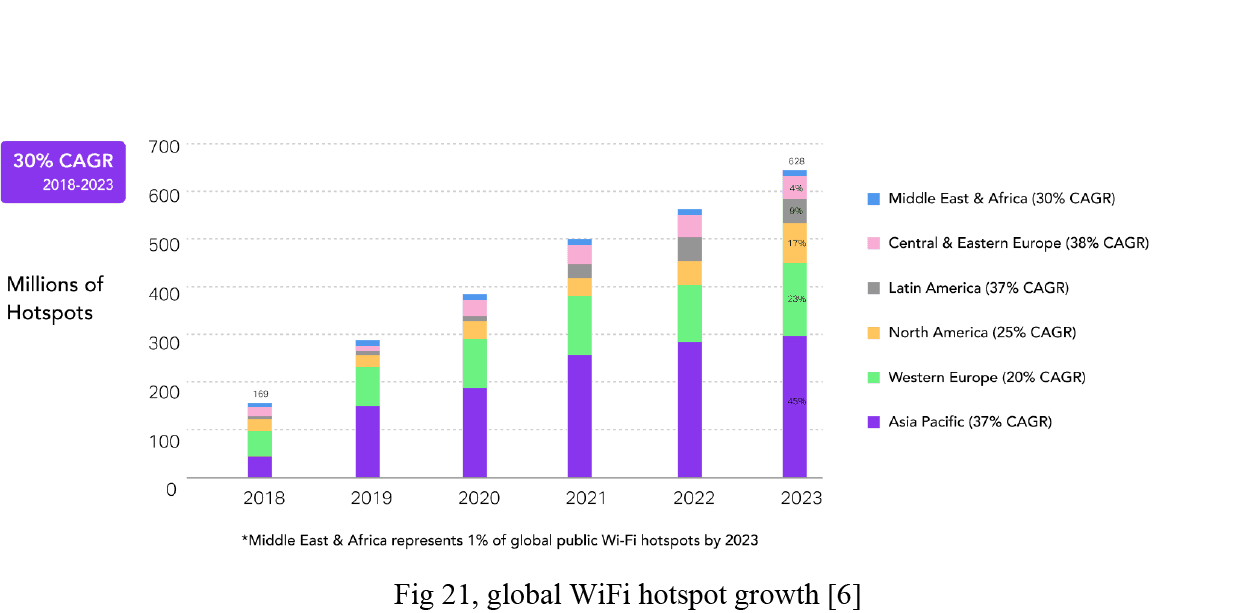

On the other hand, WiFi roaming becomes attractive as a feasible path for DeWi. First of all, telcos and mobile devices all support WiFi off-loading now. Secondly, WiFi is the most popular wireless radio access technology available, and it also has the strongest supplier chain.There are 18+ billion WiFi-enabled devices in use, and 500+ million access points are produced every year [3][6][7]. WiFi will thus support decentralized network development, as a DeWi WiFi network’s community could access the needed devices easily. Thirdly, WiFi operates in an unauthorized spectrum, and is available globally, making one global operator possible. Fourthly, WiFi does not require complex network optimization in most cases, which makes DIY and community-based deployment possible. And as explained in Section 1, after 10+ years of work by the WiFi alliance,WBA, and the entire industry, seamless global OpenRoaming is now possible, providing the foundation for decentralized global WiFi operators.

If we use the financial model described in Section 2.2 to examine decentralized cellular networks and decentralized WiFi networks, it is clear that WiFi based operators have a strong edge.

Let's re-examine this formula again:

𝑉(𝑡) = 𝑋(𝑡)∗ 𝑝(𝑡)=𝐴 ∙ 𝑛(𝑁(𝑡),𝑡)² +(𝑅 − 𝑂+𝑂′) ∙ 𝑁(𝑡) +𝑌(𝑁(𝑡),𝑡) −𝑍(𝑡)

Item 𝐴 ∙ 𝑛(𝑁(𝑡), 𝑡)² remains the same between both approaches, as the differences relate to 𝑅 and 𝑂.

𝑂 = (𝐶 + 𝐾) ∙ 𝐺 + 𝑤√𝑁 𝐹 ∙ 𝐿 − 𝑟 ⁄ 𝑁 ∆𝐷

In cellular based DeWi networks, 𝑅 refers to the data plan fees the decentralized carriers charge its customers. In the bootstrap phase, it could be considered minimum or negligible as consumers will not pay that. 𝑅 could also come from the income generated from the apps or websites related to each location. However, even if a location, like a restaurant, installs a mining rig / small cell, there has not been any business model that proves the restaurant can get any additional value from network users. With WiFi based DeWi, though, locations could charge for WiFi-based services while in most cases, the basic usage of the network could be free. However, WiFi and location based add-on services have become very mature, and are already offered in airports, railway stations, sports venues, etc. Moreover, these revenues from WiFi usage and WiFi services do not require a network effect. Even just one hotspot can create revenue. In short, at the bootstrap phase, WiFi based DeWi enables much higher revenue than cellular based DeWi.

In terms of the cost item, it is known that WiFi gateways are much cheaper than small cells, and the deployment of such devices is much lower in cost and complexity. Their operational costs - for electricity and air conditioning, for example - are lower as well. WiFi networks also do not incur any spectrum usage fees or additional regulatory charges. Though the coverage of one WiFi gateway is still less than a 5G small cell, the overall deployment costs of WiFi networks is still lower, as the interconnection between different nodes largely relies on existing ISP infrastructures. The requirements of enterprise WiFi might adversely affect this conclusion; however, Roam will minimize such an impact by reducing the costs of maintaining a complicated backend.